After writing up my first peer-to-peer presentation on personal finance for PGY’s, I decided to divide the presentation up into 2-3 posts as these slides illustrate important points.

Since high interest rate student loan is one of the MAJOR way (aside from high interest consumer/credit card debt) that time values works AGAINST us, this first post is focused on how to turn this adversity around by refinancing student loans.

{kind=link}

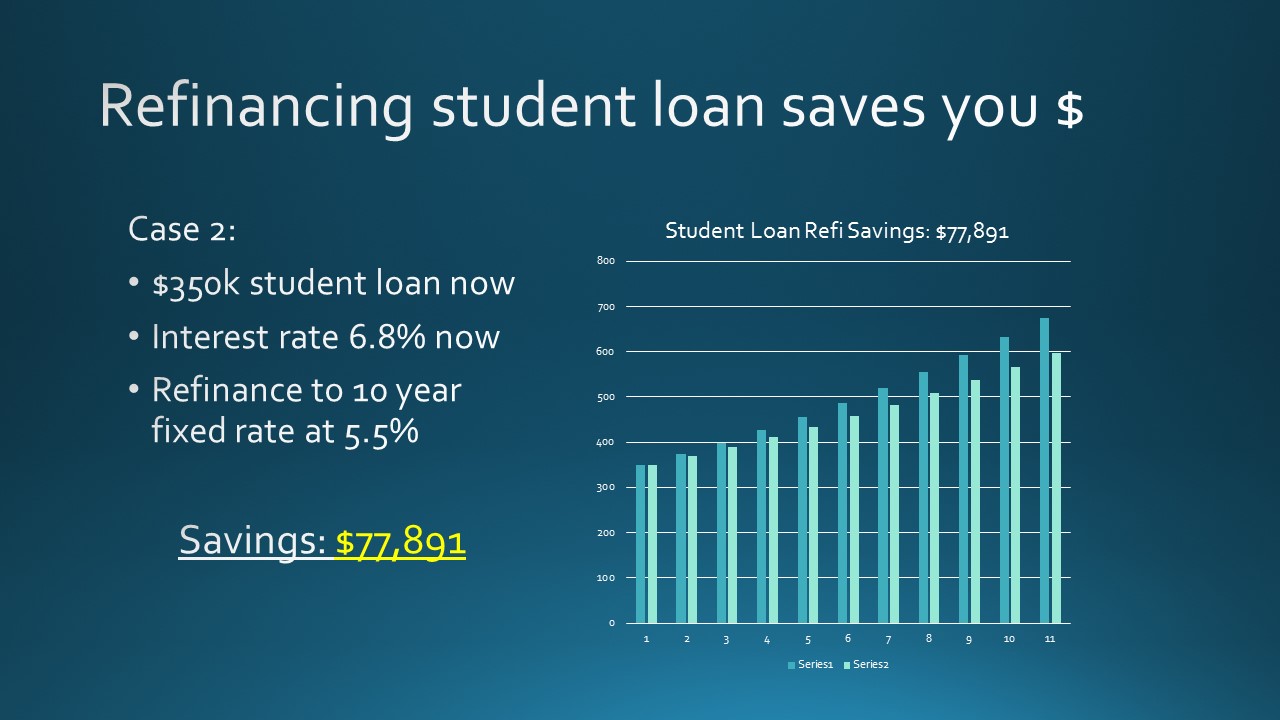

In summary, refinancing your student loan means

- lower interest rate– effortless savings

- increased cash flow–$100/mo payment in training is much less than IBR payment

- for many pgy’s, this may be the ONLY way to fund retirement/ get company match or simply to make ends meet (without dipping into more consumer debt/higher interest debt)

- the only thing you forgo is the opportunity to your loans forgiven. (except for those who are willing to limit their job options and to take a smaller paycheck working for 503c, you are not missing much.)

- For those currently deferring (not paying a dime), it sure is a deal hard to reject, when you get 40k in return for 7k investment towards your student loan (detailed in the last slide above.) i’d say yes to spending $100 less per month in a heartbeat if it meant I get nearly $500 in return for the $100 I pay towards a refinanced student loan.

- Have you refinanced your student loan(s)?

- What was your experience doing so?

- Why have you NOT refinanced your student loan(s)? How is that working out for you?

Student Loan Refinance 101

Pingback:The Student Loan Resource Page - Physician on FIRE